Sentimental Propagation Model of Stock Investors Based on Symmetric Triangular Fuzzy Set

-

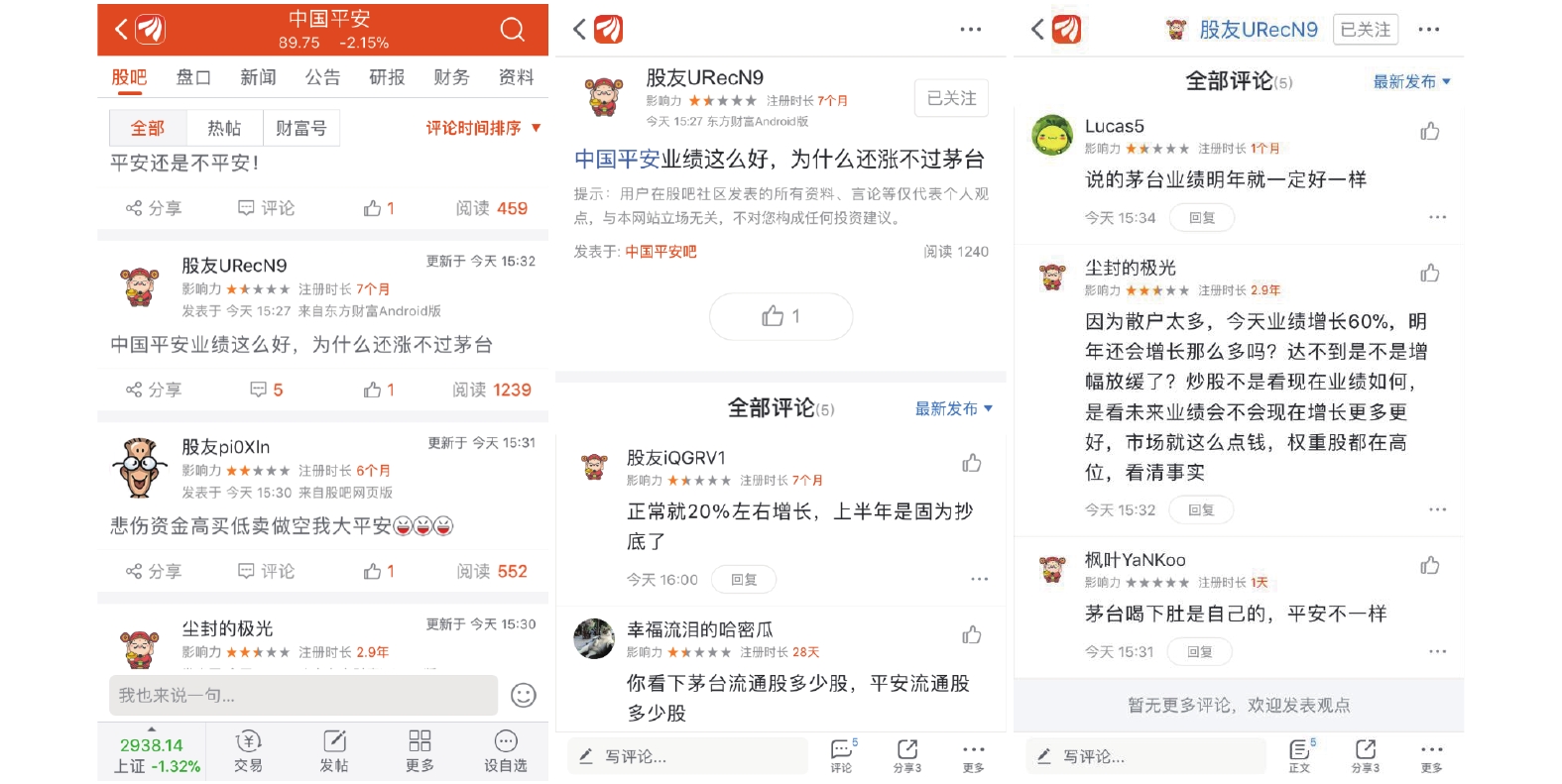

摘要: 投资者情绪是股票市场中普遍存在的一种非理性行为, 是导致股票价格波动的重要因素. 本文采用模糊集合理论, 从微观视角下研究股票投资者情绪的传播过程. 采用对称三角模糊集合描述股票投资者思维的模糊性, 用模糊股价预期表示投资者情绪, 建立了股票投资者情绪的传播模型, 提出了三种基本的投资者情绪传播方式. 以股吧社区中的投资者情绪传播为例, 说明了所提出的股票投资者情绪传播模型的有效性.Abstract: As a universal irrational behavior in stock market, investor sentiment is a significant factor leading to the fluctuation of stock price. Based on fuzzy sets theory, the propagation process of stock investor sentiment is studied from a micro perspective. The symmetrical triangular fuzzy set is used to depict fuzziness of stock investors' viewpoints, and the fuzzy stock price expectation for investor sentiment. The propagation model of stock investor sentiment is proposed, where three basic propagation types of investors' sentiment are introduced. The effectiveness of the proposed model is demonstrated via the investor sentiment propagation in the “guba”community.

-

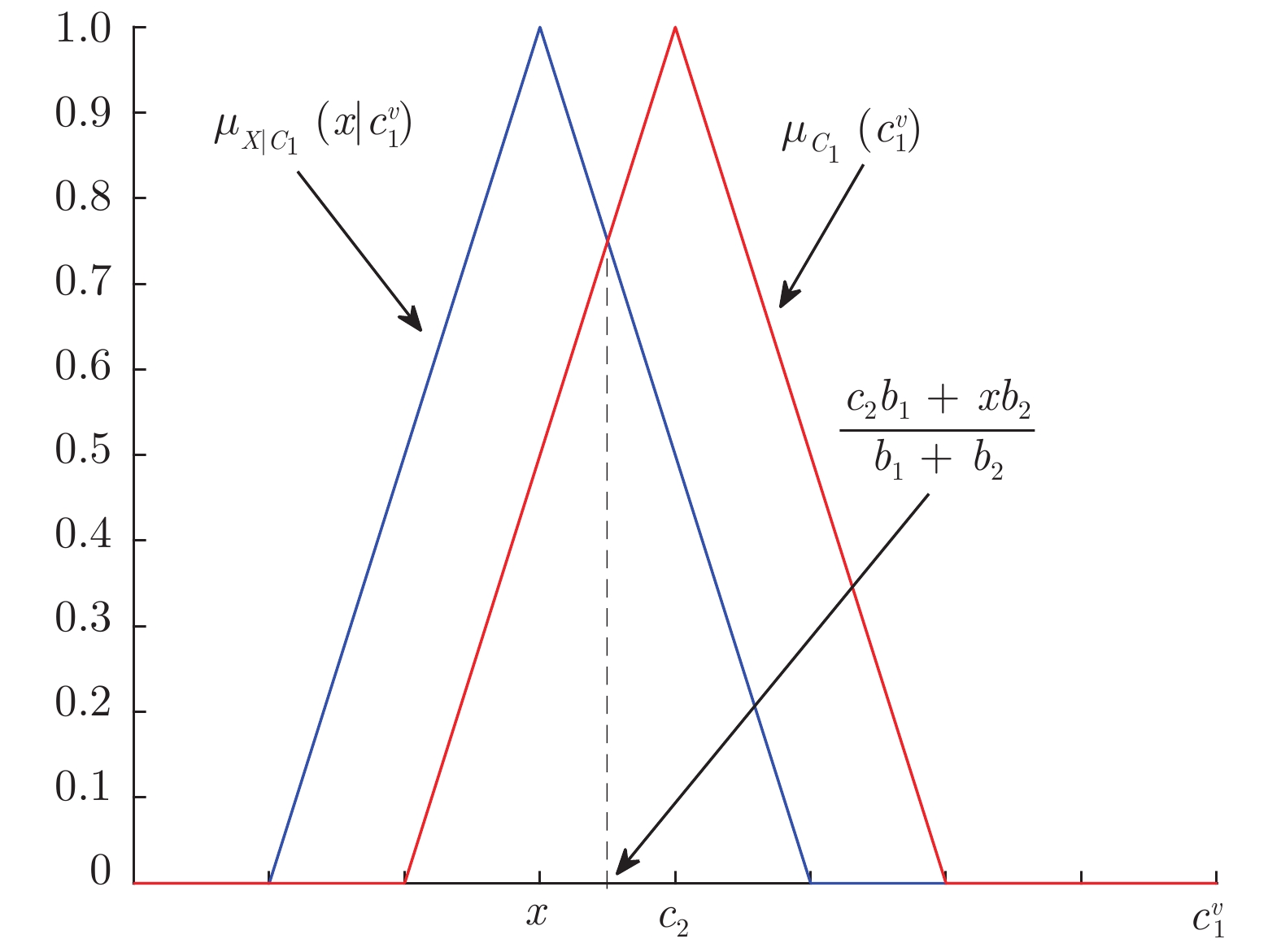

图 2 模糊股价预期中心传播时式(8)最大值的求取

Fig. 2 How the max in (8) is achieved for center propagation of fuzzy stock expectation

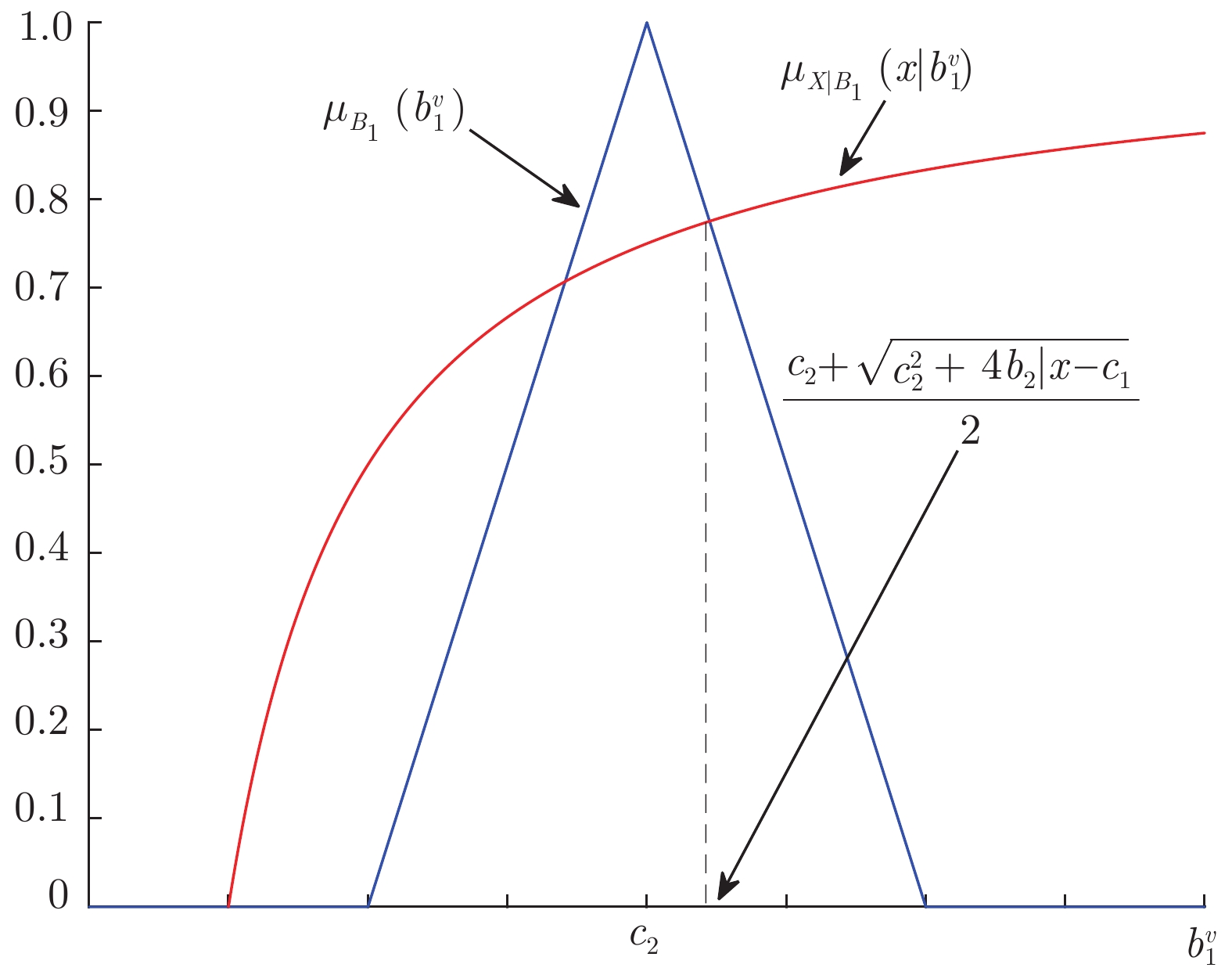

图 4 模糊股价预期不确定性传播时式(12)最大值的求取

Fig. 4 How the max in (12) is achieved for uncertainty propagation function of fuzzy stock expectation

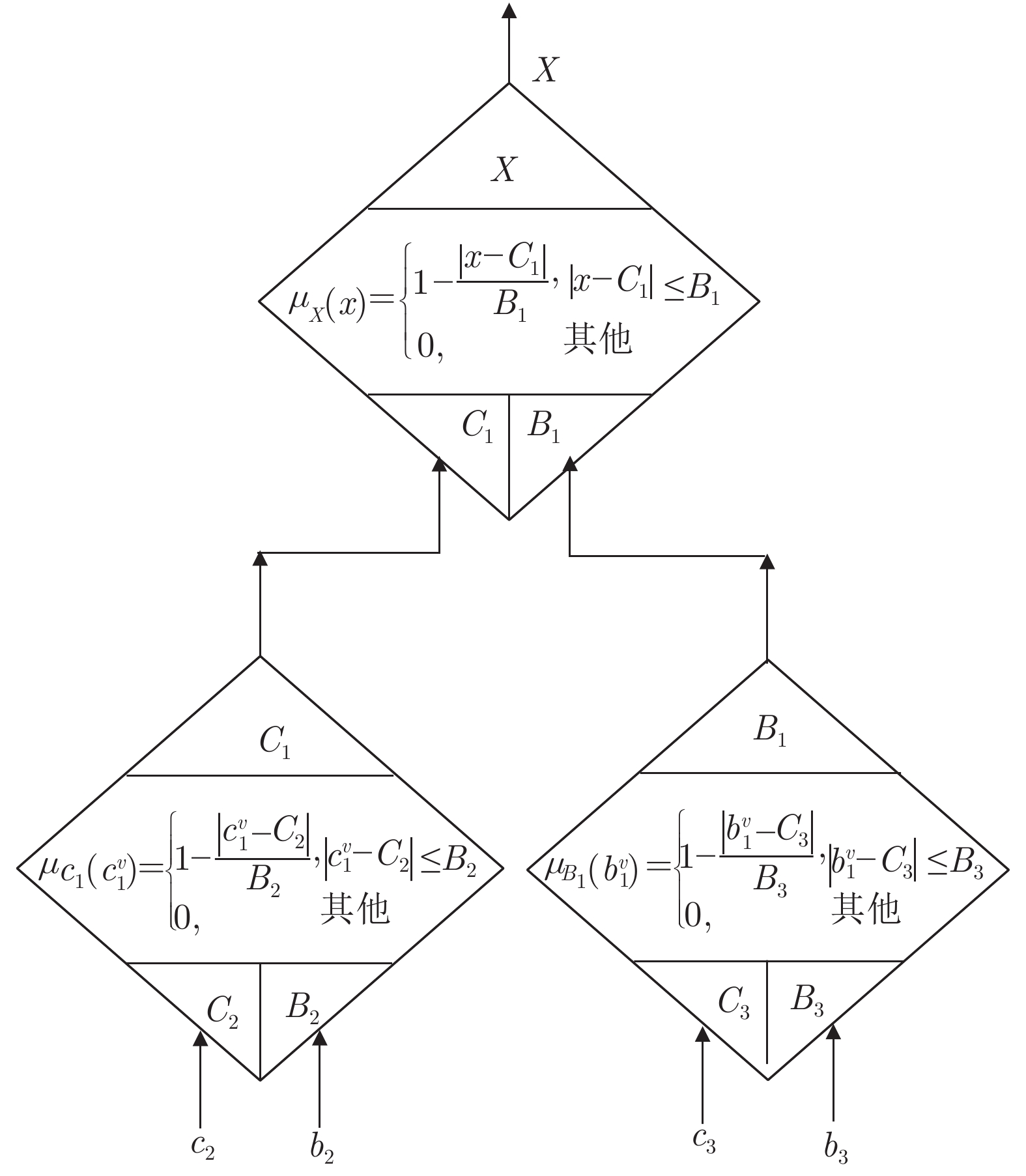

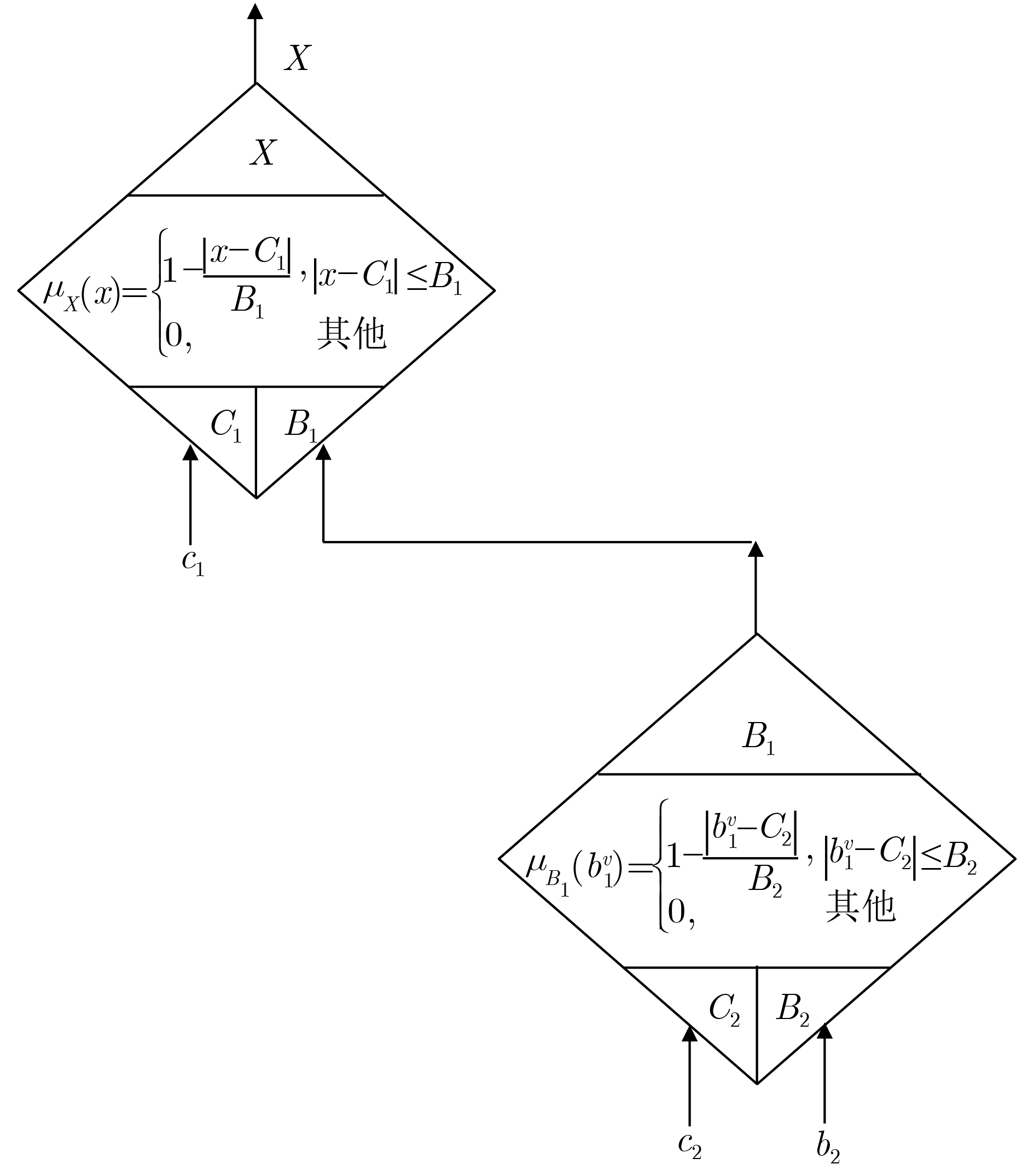

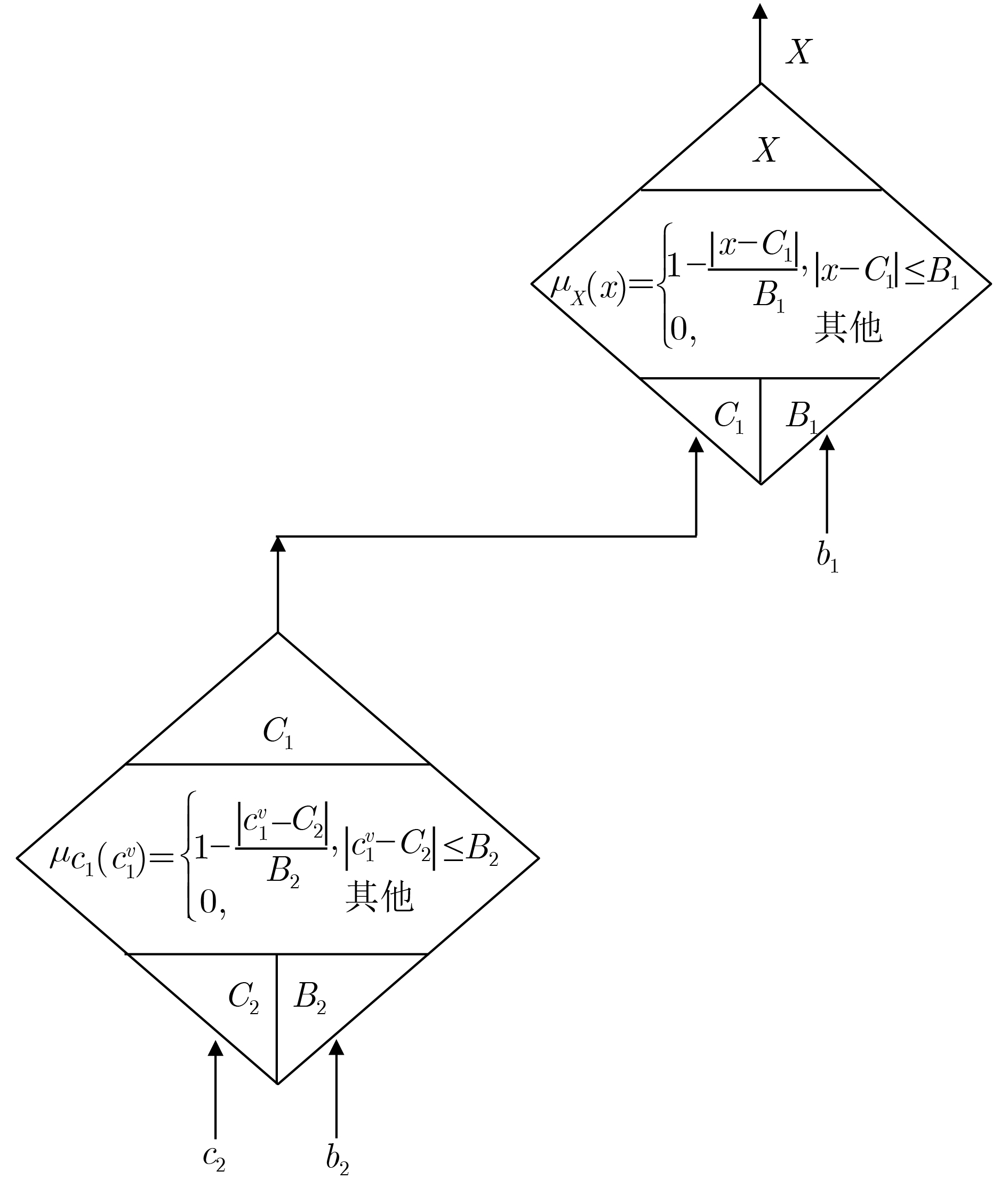

图 5 X的无条件隶属度函数

Fig. 5 Unconditional membership function of fuzzy set X under uncertainty propagation of fuzzy stock expectation

图 6 模糊股价预期中心及不确定性传播

Fig. 6 Center and uncertainty propagation of fuzzy stock expectation

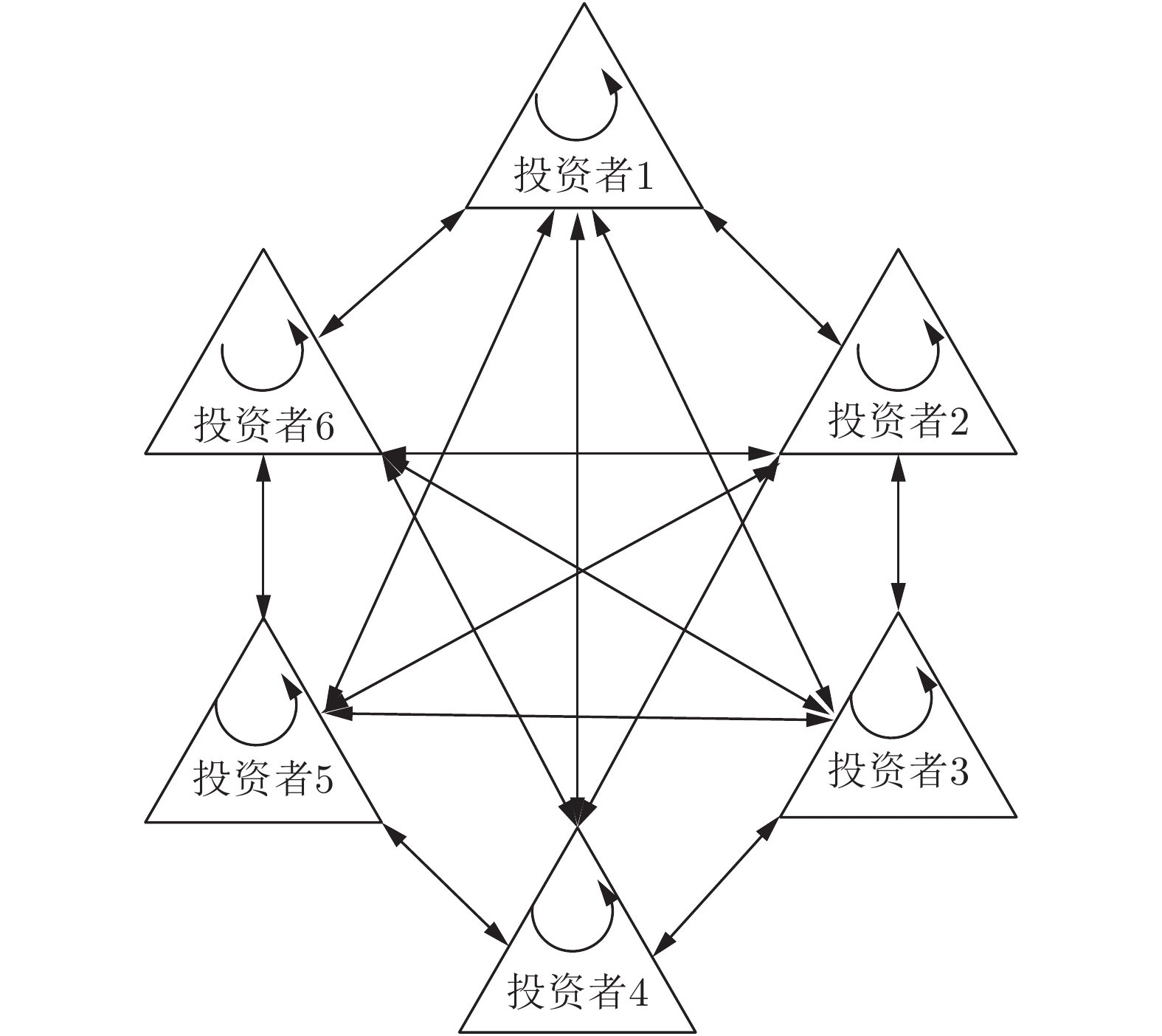

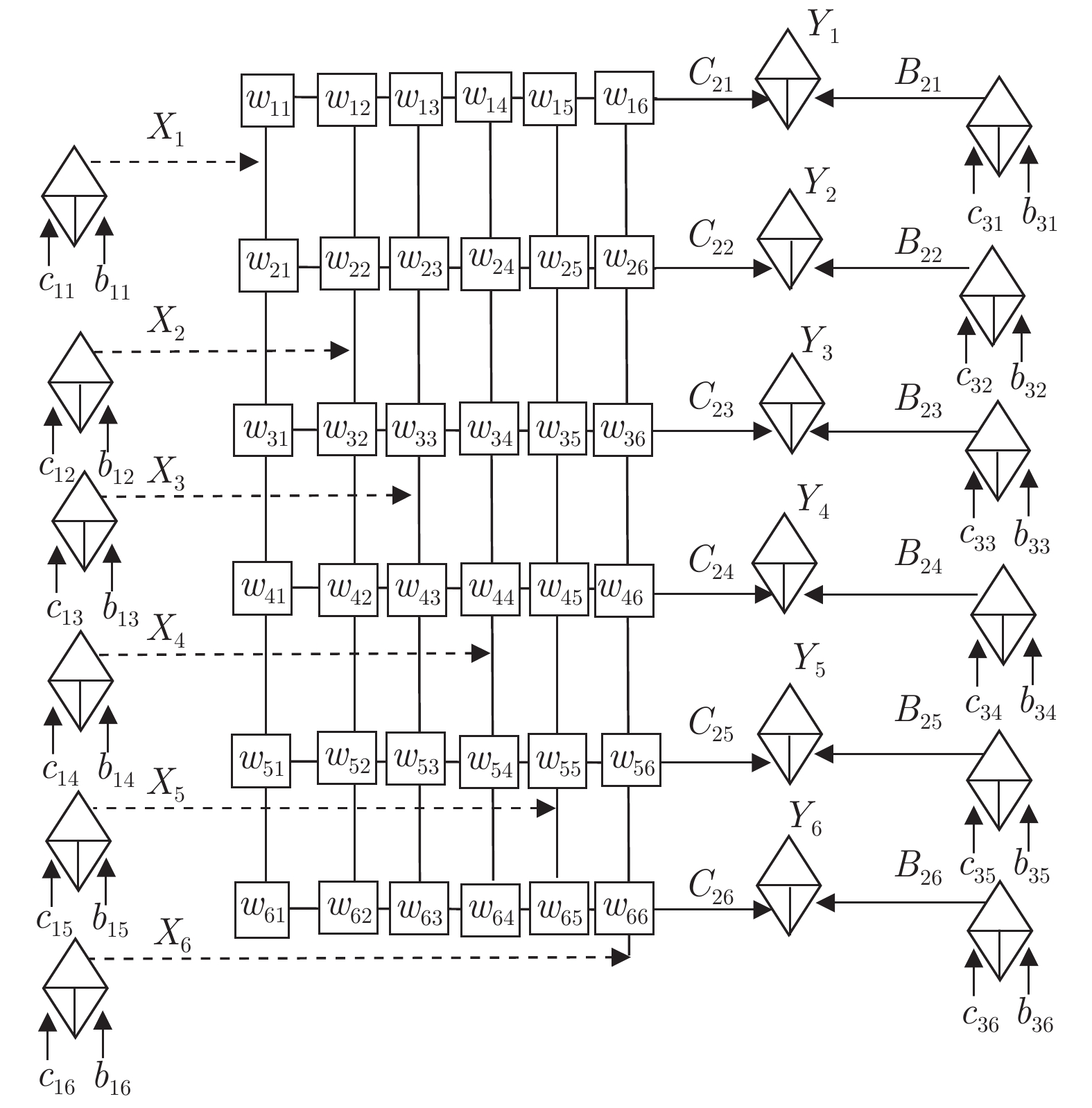

图 8 闭环投资者情绪传播示意图

Fig. 8 Close-loop network diagram of investors' sentiment propagation

-

[1] 文丹艳, 马超群, 王琨. 一种多源数据驱动的自动交易系统决策模型. 自动化学报, 2018, 44(8): 1505−1517Wen Dan-Yan, Ma Chao-Qun, Wang Kun. A multi-source data driven decision model for automatic trading systems. Acta Automatica Sinica, 2018, 44(8): 1505−1517 [2] 孙彦林, 陈守东, 刘洋. 基于股市和汇市成交量信息视角的股价波动预测. 系统工程理论与实践, 2019, 39(4): 935−945 doi: 10.12011/1000-6788-2018-1985-11Sun Yan-Lin, Chen Shou-Dong, Liu-Yang. Forecast of stock price fluctuation based on the perspective of volume information in stock and foreign exchange market. Systems Engineering-Theory & Practice, 2019, 39(4): 935−945 doi: 10.12011/1000-6788-2018-1985-11 [3] 伍燕然, 韩立岩. 不完全理性、投资者情绪与封闭式基金之谜. 经济研究, 2007, (3): 117−129Wu Yan-Ran, Han Li-Yan. Imperfect rationality, sentiment and closed-end-fund puzzle. Economic Research Journal, 2007, (3): 117−129 [4] 乌达巴拉, 汪增福. 一种基于组合语义的文本情绪分析模型. 自动化学报, 2015, 41(12): 2125−2137Odbal, Wang Zeng-Fu. Emotion analysis model using compositional semantics. Acta Automatica Sinica, 2015, 41(12): 2125−2137 [5] 郭东伟, 乌云娜, 邹蕴, 孟祥燕. 基于非理性博弈的舆情传播仿真建模研究. 自动化学报, 2014, 40(8): 1721−1732Guo Dong-Wei, Wu Yun-Na, Zou Yun, Meng Xiang-Yan. Simulation and modeling of non-rational game based public opinion spread. Acta Automatica Sinica, 2014, 40(8): 1721−1732 [6] 部慧, 解峥, 李佳鸿. 基于股评的投资者情绪对股票市场的影响. 管理科学学报, 2018, 21(4): 91−106Bu Hui, Xie Zheng, Li Jia-Hong. Investor sentiment extracted from internet stock message boards and its effect on Chinese stock market. Journal of Management Sciences in China, 2018, 21(4): 91−106 [7] Sul H K, Dennis A R, Yuan L. Trading on Twitter: using social media sentiment to predict stock returns. Decision Sciences, 2017, 48(3): 454−488 doi: 10.1111/deci.12229 [8] 许启发, 伯仲璞, 蒋翠侠. 基于分位数Granger因果的网络情绪与股市收益关系研究. 管理科学, 2017, 30(3): 147−160 doi: 10.3969/j.issn.1672-0334.2017.03.013Xu Qi-Fa, Bo Zhong-Pu, Jiang Cui-Xia. Exploring the relationship between Internet sentiment and stock market returns based on quantile granger causality analysis. Journal of Management Science, 2017, 30(3): 147−160 doi: 10.3969/j.issn.1672-0334.2017.03.013 [9] Scott J. Social Network Analysis (4th Edition), London, U.K.: Sage Publications Ltd, 2017. [10] Acemoglu D, Ozdaglar A. Opinion dynamics and learning in social networks. Dynamic Games and Applications, 2011, 1(1): 3−49 doi: 10.1007/s13235-010-0004-1 [11] Yuan Y. Market-wide attention, trading, and stock returns. Journal of Financial Economics, 2015, 116(3): 548−564 doi: 10.1016/j.jfineco.2015.03.006 [12] 吴璇, 田高良, 司毅. 网络舆情管理与股票流动性. 管理科学, 2017, 30(6): 51−64 doi: 10.3969/j.issn.1672-0334.2017.06.004Wu Xuan, Tian Gao-Liang, Si Yi. Internet media management and stock liquidity. Journal of Management Science, 2017, 30(6): 51−64 doi: 10.3969/j.issn.1672-0334.2017.06.004 [13] Bozorgi A, Samet S, Kwisthout J, Wareham T. Community-based influence maximization in social networks under a competitive linear threshold model. Knowledge-Based Systems, 2017, 134: 149−158 doi: 10.1016/j.knosys.2017.07.029 [14] Zhang X, Jiang D, Alsaedi A, Hayat T. Stationary distribution of stochastic SIS epidemic model with vaccination under regime switching. Applied Mathematics Letters, 2016, 59: 87−93 doi: 10.1016/j.aml.2016.03.010 [15] 熊熙, 乔少杰, 吴涛, 吴越, 韩楠, 张海清. 基于时空特征的社交网络情绪传播分析与预测模型. 自动化学报, 2018, 44(12): 2290−2299Xiong Xi, Qiao Shao-Jie, Wu Tao, Wu Yue, Han Nan, Zhang Hai-Qing. Spatio-temporal feature based emotional contagion analysis and prediction model for online social networks. Acta Automatica Sinica, 2018, 44(12): 2290−2299 [16] Liu X, He D, Liu C. Information diffusion nonlinear dynamics modeling and evolution analysis in online social network based on emergency events. IEEE Transactions on Computational Social Systems, 2019, 6(1): 8−19 doi: 10.1109/TCSS.2018.2885127 [17] Zhuang Y, Yagan O. Information propagation in clustered multilayer networks. IEEE Transactions on Network Science and Engineering, 2016, 3(4): 211−224 doi: 10.1109/TNSE.2016.2600059 [18] Jackson M O. Social and Economic Networks. Princeton, NJ, USA: Princeton University Press, 2008 [19] Wang L X, Mendel J M. Fuzzy opinion networks: a mathematical framework for the evolution of opinions and their uncertainties across social networks. IEEE Transactions on Fuzzy Systems, 2016, 24(4): 880−905 doi: 10.1109/TFUZZ.2015.2486816 [20] Wang L X, Mendel J M. Fuzzy networks: What happens when fuzzy people are connected through social networks. In: Proceedings of the 2014 IEEE Symposium on Foundations of Comput-ational Intelligence (FOCI). Orlando, FL, USA: IEEE, 2014. 30-37 [21] Wang L X. Hierarchical fuzzy opinion networks: top-down for social organizations and bottom-up for election. arXiv preprint, arXiv: 1901.00441, 2019 [22] Hommes C H. Heterogeneous agent models in economics and finance. Handbook of Computational Economics, 2006, 2: 1109-1186 [23] Wang L X. Modeling stock price dynamics with fuzzy opinion networks. IEEE Transactions on Fuzzy Systems, 2017, 25(2): 277−301 doi: 10.1109/TFUZZ.2016.2574911 [24] Lux T. Estimation of an agent-based model of investor sentiment formation in financial markets. Journal of Economic Dynamics and Control, 2012, 36(8): 1284−1302 doi: 10.1016/j.jedc.2012.03.012 [25] Anzilli L, Facchinetti G. A Fuzzy quantity mean-variance view and its application to a client financial risk tolerance model. International Journal of Intelligent Systems, 2016, 31(10): 963−988 doi: 10.1002/int.21812 [26] Chen H M, Hu C F, Yeh W C. Option pricing and the greeks under gaussian fuzzy environments. Soft Computing, 2019, 23(24): 13351−13374 doi: 10.1007/s00500-019-03876-w [27] Baker M P, Wurgler J. Investor dentiment and the cross-section of stock returns. Economic Management Journal, 2006, 61(4): 1645−1680 [28] Da Z, Engelberg J, Gao P. The sum of all FEARS investor sentiment and asset prices. Review of Financial Studies, 2014, 28(1): 1−32 [29] Zadeh L A. Is there a need for fuzzy logic? Information Sciences, 2008, 178(13): 2751−2779 [30] Zadeh L A. Outline of new approach to the analysis of complex systems and decision processes. IEEE Transaction Systems, Man, and Cybernetics, 1973, SMC-3(1): 28−44 doi: 10.1109/TSMC.1973.5408575 [31] Zadeh L A. The concept of a linguistic variable and its application to approximate reasoning-I. Information Sciences, 1975, 8(3): 199−249 doi: 10.1016/0020-0255(75)90036-5 -

下载:

下载:

点击查看大图

点击查看大图

计量

- 文章访问数: 1909

- HTML全文浏览量: 1090

- PDF下载量: 143

- 被引次数: 0